Quantitative evaluation of the investment in a renewable energy project relies on a series of factors and metrics. These elements differ based on the stakeholder role as each has a different risk-reward expectation and its own metrics to assess project return. For example:

- A debt provider (lender) will surveil the project’s ability to generate enough revenues to cover its debt (plus interest) as well as operational costs, taxes.

- The project developer (equity investor) will look at metrics such as the Equity Internal Rate of Return (IRR), Project IRR and the Net Present Value (NPV).

Let’s start with the definition of these elements before shifting to minimum profitability values.

The Net Present Value (NPV)

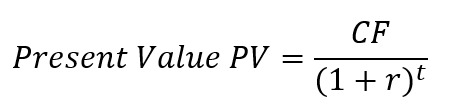

As renewable energy investments are usually long-term ones, risk and time need to be considered due to the impact they have on the value of money. That’s why we talk about Present Value PV (or Discounted Value).

Let’s make it easy: a one-dollar bill has more value today than the next week (or day, or month). With today’s dollar, one can generate additional profit and avoid a loss of opportunity. Today’s dollar is a secure fund that would allow returns with more security than next week’s dollar, a less secure return. So, time and risk properties have to be included in the assessment of a particular investment at a given time.

To calculate the Discounted Value (PV), a risk-based interest rate must be applied to the project’s future cash flows (CF): the riskier a project is, the higher the interest rate r is as investor need to mitigate investment risks. Present Value is calculated as follows:

Where:

- PV is the present value

- CF is the project cashflow

- r is the discount rate

- t is the year over which the PV is being calculated

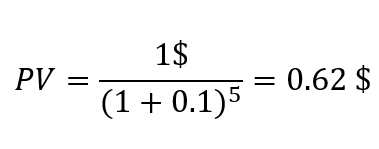

Let’s get back to the one-dollar example. If I receive a dollar in year 5 with a 10% annual interest rate, its present value will be equal to:

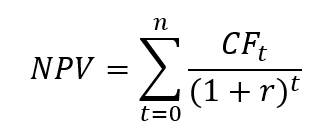

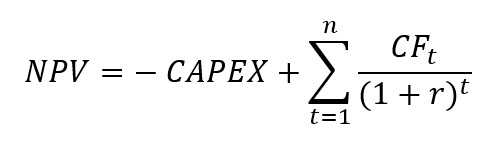

The Net Present Value is the sum of all project expenses and revenues that allow the initial expenditures (CAPEX) to be repaid and keep it operational (OPEX) to generate revenues. The NPV is calculated as follows:

Where:

- NPV is the net present value

- CF is the project cashflow equal to revenues minus expenses

- r is the discount rate

- t is the year over which the NPV is being calculated

Supposing that the project is paid in year 0 (in the beginning of the project) through an initial investment CAPEX and revenues start in Year 1, the NPV is:

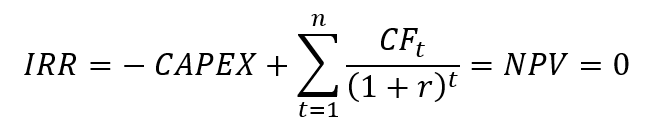

Internal Rate of Return (IRR)

The IRR is the average periodical revenue produced by the cashflow of a project compared to its investment. The IRR is equivalent to the discount rate r that gives an NPV close to zero.

The different types of IRR

The Blend IRR term is often used to refer to the fact that equity placements by investors are often presented under a subordinated debt instead of purchasing shares in the project or project company.

As shareholder revenues (such as dividends) are subjected to taxes, subordinated debt are often sough after as they are exempted from taxes. This approach preserves the priority of payment for both equity investors and lenders: senior debt will still be paid first then equity distribution among shareholders and subordinated debt lenders follows.

As the taxable part under the Blend IRR (dividends) is relatively small when compared to other elements, pre-tax and post-tax Blend IRR values are intimately close.

Project IRR

The project IRR is simply limited to the measure of a project’s return of the money that was invested without considering its source (equity or debt). It is based on the project’s cashflow before any debt repayment or dividend distribution.

This measure gives a high-level indication of a project’s return. Another unit, called Equity IRR help cover such shortfalls.

Equity IRR

The Equity IRR assesses the return of invested equity and relies on the debt leverage. As it is sensitive to the debt leverage, the Equity IRR needs to cover the debt and equity contributions. The Equity IRR is evaluated only with the equity part of the initial investment and future equity cashflows considering debt repayment (CFADS – DS).

A project that fully relies on equity has an equity IRR equal to the project IRR.

Debt and Leverage

An important parameter of a renewable energy project is the debt-to-equity ratio (or gearing) in the investment. For example, a project located within a high-credit rated country with a secure offtake contract would see lenders covering up to 80% of the investment: an 80:20 ratio. If the same project was located within a geography with higher economic risks, this ratio would be of 70:20 in most optimistic cases with shorter loan duration and higher interest rates.

Usually, the project owner will seek to maximize profits and minimize the use of its own funds hence looks for a larger debt to finance its project. Usually, the larger the debt is, the better it is as interest rates remain lower than the opportunity cost of equity money that could be mobilized in other opportunities.